Levy Stable 随机波动率模型¶

本教程通过一个非高斯随机波动率模型的示例,演示了如何使用 Levy Stable 分布进行推理。

Stable 分布的推理非常棘手,因为其密度函数 Stable.log_prob() 计算成本很高。在本教程中,我们将演示三种推理方法:(i) 使用 poutine.reparam 效应将模型转换为可处理的形式,(ii) 在 SVI 中使用无似然损失 EnergyDistance,以及 (iii) 使用包含数值积分对数概率计算的 Stable.log_prob()。

总结¶

Stable.log_prob() 计算成本很高。

Stable 分布的推理需要重参数化或无似然损失。

重参数化

poutine.reparam() handler 可以使用各种策略转换模型。

StableReparam 策略可用于 SVI 或 HMC 中的 Stable 分布。

LatentStableReparam 策略成本稍低,但不能用于似然。

DiscreteCosineReparam 策略可以改善批量潜在时间序列模型的几何形状。

使用 SVI 的无似然损失

EnergyDistance 损失允许在 guide 和模型似然中使用 Stable 分布。

目录¶

使用

EnergyDistance对对数收益率拟合单个分布使用以下方法建模随机波动率

每日 S&P 500 数据¶

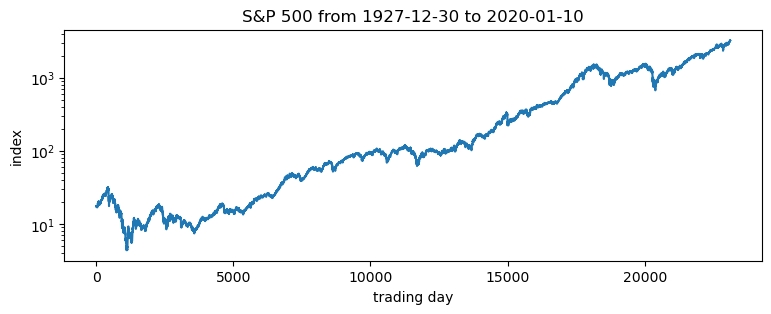

以下 S&P 500 每日收盘价从 Yahoo finance 加载。

[1]:

import math

import os

import torch

import pyro

import pyro.distributions as dist

from matplotlib import pyplot

from torch.distributions import constraints

from pyro import poutine

from pyro.contrib.examples.finance import load_snp500

from pyro.infer import EnergyDistance, Predictive, SVI, Trace_ELBO

from pyro.infer.autoguide import AutoDiagonalNormal

from pyro.infer.reparam import DiscreteCosineReparam, StableReparam

from pyro.optim import ClippedAdam

from pyro.ops.tensor_utils import convolve

%matplotlib inline

assert pyro.__version__.startswith('1.9.1')

smoke_test = ('CI' in os.environ)

[2]:

df = load_snp500()

dates = df.Date.to_numpy()

x = torch.tensor(df["Close"]).float()

x.shape

[2]:

torch.Size([23116])

[3]:

pyplot.figure(figsize=(9, 3))

pyplot.plot(x)

pyplot.yscale('log')

pyplot.ylabel("index")

pyplot.xlabel("trading day")

pyplot.title("S&P 500 from {} to {}".format(dates[0], dates[-1]));

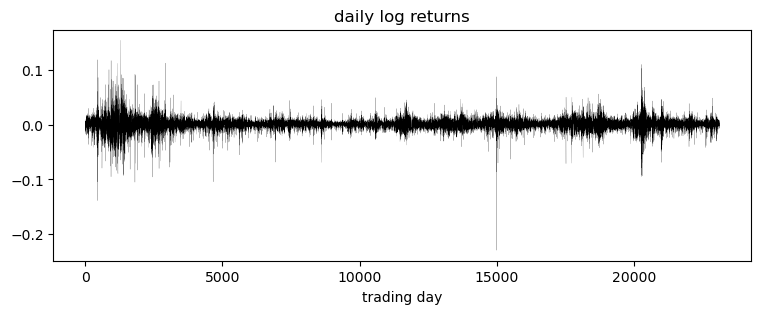

感兴趣的是对数收益率,即连续两天价格对数比率。

[4]:

pyplot.figure(figsize=(9, 3))

r = (x[1:] / x[:-1]).log()

pyplot.plot(r, "k", lw=0.1)

pyplot.title("daily log returns")

pyplot.xlabel("trading day");

[5]:

pyplot.figure(figsize=(9, 3))

pyplot.hist(r.numpy(), bins=200)

pyplot.yscale('log')

pyplot.ylabel("count")

pyplot.xlabel("daily log returns")

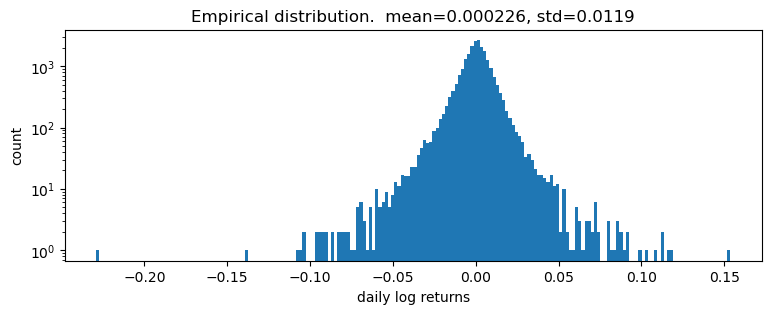

pyplot.title("Empirical distribution. mean={:0.3g}, std={:0.3g}".format(r.mean(), r.std()));

对对数收益率拟合单个分布¶

对数收益率似乎具有重尾。首先,我们尝试对收益率拟合单个分布。为了拟合分布,我们将使用无似然统计推理算法 EnergyDistance,该算法匹配观测数据的分数矩,并且可以处理重尾数据。

[6]:

def model():

stability = pyro.param("stability", torch.tensor(1.9),

constraint=constraints.interval(0, 2))

skew = 0.

scale = pyro.param("scale", torch.tensor(0.1), constraint=constraints.positive)

loc = pyro.param("loc", torch.tensor(0.))

with pyro.plate("data", len(r)):

return pyro.sample("r", dist.Stable(stability, skew, scale, loc), obs=r)

[7]:

%%time

pyro.clear_param_store()

pyro.set_rng_seed(1234567890)

num_steps = 1 if smoke_test else 201

optim = ClippedAdam({"lr": 0.1, "lrd": 0.1 ** (1 / num_steps)})

svi = SVI(model, lambda: None, optim, EnergyDistance())

losses = []

for step in range(num_steps):

loss = svi.step()

losses.append(loss)

if step % 20 == 0:

print("step {} loss = {}".format(step, loss))

print("-" * 20)

pyplot.figure(figsize=(9, 3))

pyplot.plot(losses)

pyplot.yscale("log")

pyplot.ylabel("loss")

pyplot.xlabel("SVI step")

for name, value in sorted(pyro.get_param_store().items()):

if value.numel() == 1:

print("{} = {:0.4g}".format(name, value.squeeze().item()))

step 0 loss = 7.497945785522461

step 20 loss = 2.0790653228759766

step 40 loss = 1.6773109436035156

step 60 loss = 1.4146158695220947

step 80 loss = 1.306936502456665

step 100 loss = 1.2835698127746582

step 120 loss = 1.2812254428863525

step 140 loss = 1.2803162336349487

step 160 loss = 1.2787212133407593

step 180 loss = 1.265405535697937

step 200 loss = 1.2878881692886353

--------------------

loc = 0.0002415

scale = 0.008325

stability = 1.982

CPU times: total: 828 ms

Wall time: 2.93 s

[8]:

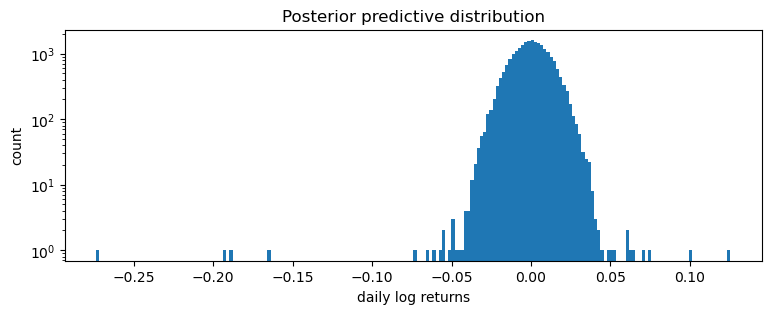

samples = poutine.uncondition(model)().detach()

pyplot.figure(figsize=(9, 3))

pyplot.hist(samples.numpy(), bins=200)

pyplot.yscale("log")

pyplot.xlabel("daily log returns")

pyplot.ylabel("count")

pyplot.title("Posterior predictive distribution");

这是一个糟糕的拟合,但这在意料之中,因为我们将所有时间步混合在一起:我们期望这是一个分布(Normal 或 Stable)的尺度混合,但却将其建模为单个分布(在本例中为 Stable)。

建模随机波动率¶

接下来我们将拟合一个随机波动率模型。让我们从一个恒定波动率模型开始,其中对数价格 \(p\) 遵循布朗运动

其中 \(w_t\) 是一系列标准白噪声。我们可以将此模型重写为对数收益率 \(r_t=\log(p_t\,/\,p_{t-1})\) 的形式

现在为了解释波动率聚集,我们可以泛化到随机波动率模型,其中波动率 \(h\) 取决于时间 \(t\)。最简单的此类模型之一是 \(h_t\) 遵循几何布朗运动

其中 \(v_t\) 再次是一系列标准白噪声。因此,整个模型包含一个几何布朗运动 \(h_t\),它确定了另一个几何布朗运动 \(p_t\) 的扩散率

通常 \(v_1\) 和 \(w_t\) 都是高斯分布。我们将 \(w_t\) 泛化为 Stable 分布,学习三个参数(稳定性、偏度和位置),但仍然按 \(\sqrt h_t\) 进行缩放。

我们的 Pyro 模型将对增量 \(v_t\) 进行采样,并通过 pyro.deterministic 记录 \(\log h_t\) 的计算。请注意,在 Pyro 中实现此模型有许多方法,并且几何形状可能因实现而异。以下版本与重参数化器结合使用时,似乎具有良好的几何形状。

[9]:

def model(data):

# Note we avoid plates because we'll later reparameterize along the time axis using

# DiscreteCosineReparam, breaking independence. This requires .unsqueeze()ing scalars.

h_0 = pyro.sample("h_0", dist.Normal(0, 1)).unsqueeze(-1)

sigma = pyro.sample("sigma", dist.LogNormal(0, 1)).unsqueeze(-1)

v = pyro.sample("v", dist.Normal(0, 1).expand(data.shape).to_event(1))

log_h = pyro.deterministic("log_h", h_0 + sigma * v.cumsum(dim=-1))

sqrt_h = log_h.mul(0.5).exp().clamp(min=1e-8, max=1e8)

# Observed log returns, assumed to be a Stable distribution scaled by sqrt(h).

r_loc = pyro.sample("r_loc", dist.Normal(0, 1e-2)).unsqueeze(-1)

r_skew = pyro.sample("r_skew", dist.Uniform(-1, 1)).unsqueeze(-1)

r_stability = pyro.sample("r_stability", dist.Uniform(0, 2)).unsqueeze(-1)

pyro.sample("r", dist.Stable(r_stability, r_skew, sqrt_h, r_loc * sqrt_h).to_event(1),

obs=data)

使用重参数化拟合模型¶

我们使用两个重参数化器:StableReparam 用于处理 Stable 似然(因为 Stable.log_prob() 计算成本很高),以及 DiscreteCosineReparam 用于改善潜在高斯过程 v 的几何形状。然后我们将 reparam_model 用于推理和预测。

[10]:

reparam_model = poutine.reparam(model, {"v": DiscreteCosineReparam(),

"r": StableReparam()})

[11]:

%%time

pyro.clear_param_store()

pyro.set_rng_seed(1234567890)

def fit_model(model):

num_steps = 1 if smoke_test else 3001

optim = ClippedAdam({"lr": 0.05, "betas": (0.9, 0.99), "lrd": 0.1 ** (1 / num_steps)})

guide = AutoDiagonalNormal(model)

svi = SVI(model, guide, optim, Trace_ELBO())

losses = []

stats = []

for step in range(num_steps):

loss = svi.step(r) / len(r)

losses.append(loss)

stats.append(guide.quantiles([0.325, 0.675]).items())

if step % 200 == 0:

median = guide.median()

print("step {} loss = {:0.6g}".format(step, loss))

return guide, losses, stats

guide, losses, stats = fit_model(reparam_model)

print("-" * 20)

for name, (lb, ub) in sorted(stats[-1]):

if lb.numel() == 1:

lb = lb.squeeze().item()

ub = ub.squeeze().item()

print("{} = {:0.4g} ± {:0.4g}".format(name, (lb + ub) / 2, (ub - lb) / 2))

pyplot.figure(figsize=(9, 3))

pyplot.plot(losses)

pyplot.ylabel("loss")

pyplot.xlabel("SVI step")

pyplot.xlim(0, len(losses))

pyplot.ylim(min(losses), 20)

step 0 loss = 2244.54

step 200 loss = -1.16091

step 400 loss = -2.96091

step 600 loss = -3.01823

step 800 loss = -3.03623

step 1000 loss = -3.04261

step 1200 loss = -3.07324

step 1400 loss = -3.06965

step 1600 loss = -3.08399

step 1800 loss = -3.08298

step 2000 loss = -3.08325

step 2200 loss = -3.09142

step 2400 loss = -3.09739

step 2600 loss = -3.10487

step 2800 loss = -3.09952

step 3000 loss = -3.10444

--------------------

h_0 = -0.2587 ± 0.00434

r_loc = 0.04707 ± 0.002965

r_skew = 0.001134 ± 0.0001323

r_stability = 1.946 ± 0.001327

sigma = 0.1359 ± 6.603e-05

CPU times: total: 19.7 s

Wall time: 2min 54s

[11]:

(-3.119090303321589, 20.0)

对数收益率似乎表现出非常小的偏度,但稳定性参数略低于 2,且具有显著差异。这与通常对应于偏度=0 和稳定性=2 的 Normal 模型形成对比。我们现在可以可视化估计的波动率

[12]:

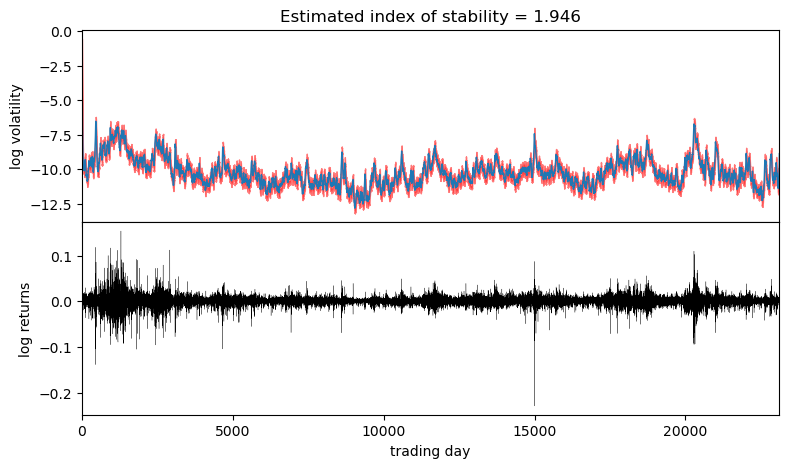

fig, axes = pyplot.subplots(2, figsize=(9, 5), sharex=True)

pyplot.subplots_adjust(hspace=0)

axes[1].plot(r, "k", lw=0.2)

axes[1].set_ylabel("log returns")

axes[1].set_xlim(0, len(r))

# We will pull out median log returns using the autoguide's .median() and poutines.

num_samples = 200

with torch.no_grad():

pred = Predictive(reparam_model, guide=guide, num_samples=num_samples, parallel=True)(r)

log_h = pred["log_h"]

axes[0].plot(log_h.median(0).values, lw=1)

axes[0].fill_between(torch.arange(len(log_h[0])),

log_h.kthvalue(int(num_samples * 0.1), dim=0).values,

log_h.kthvalue(int(num_samples * 0.9), dim=0).values,

color='red', alpha=0.5)

axes[0].set_ylabel("log volatility")

stability = pred["r_stability"].median(0).values.item()

axes[0].set_title("Estimated index of stability = {:0.4g}".format(stability))

axes[1].set_xlabel("trading day");

观察到波动率大致遵循对数收益率绝对值较大的区域。请注意,由于我们使用了近似的 AutoDiagonalNormal guide,因此不确定性被低估了。为了获得更精确的不确定性估计,可以使用 HMC 或 NUTS 推理。

使用数值积分对数概率拟合模型¶

我们现在创建一个没有对 Stable 分布进行重参数化的模型。该模型将使用 Stable.log_prob() 方法来计算对数概率密度。

[13]:

from functools import partial

model_with_log_prob = poutine.reparam(model, {"v": DiscreteCosineReparam()})

[14]:

%%time

pyro.clear_param_store()

pyro.set_rng_seed(1234567890)

guide_with_log_prob, losses_with_log_prob, stats_with_log_prob = fit_model(model_with_log_prob)

print("-" * 20)

for name, (lb, ub) in sorted(stats_with_log_prob[-1]):

if lb.numel() == 1:

lb = lb.squeeze().item()

ub = ub.squeeze().item()

print("{} = {:0.4g} ± {:0.4g}".format(name, (lb + ub) / 2, (ub - lb) / 2))

pyplot.figure(figsize=(9, 3))

pyplot.plot(losses_with_log_prob)

pyplot.ylabel("loss")

pyplot.xlabel("SVI step")

pyplot.xlim(0, len(losses_with_log_prob))

pyplot.ylim(min(losses_with_log_prob), 20)

step 0 loss = 10.872

step 200 loss = -3.21741

step 400 loss = -3.28172

step 600 loss = -3.28264

step 800 loss = -3.28722

step 1000 loss = -3.29258

step 1200 loss = -3.28663

step 1400 loss = -3.30035

step 1600 loss = -3.29928

step 1800 loss = -3.30102

step 2000 loss = -3.30336

step 2200 loss = -3.30392

step 2400 loss = -3.30549

step 2600 loss = -3.30622

step 2800 loss = -3.30624

step 3000 loss = -3.30575

--------------------

h_0 = -0.2038 ± 0.005494

r_loc = 0.04509 ± 0.003355

r_skew = -0.09735 ± 0.02454

r_stability = 1.918 ± 0.002963

sigma = 0.1391 ± 6.794e-05

CPU times: total: 1h 20min 43s

Wall time: 1h 7s

[14]:

(-3.3079991399111877, 20.0)

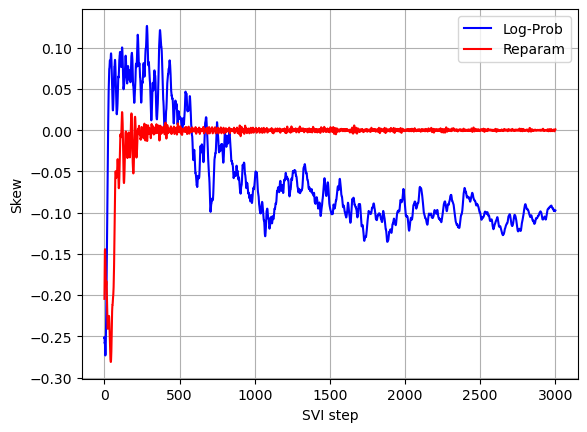

对数收益率表现出负偏度,这在使用 Stable 分布重参数化的模型中没有被捕捉到。负偏度意味着负对数收益率的尾部比正对数收益率的尾部更重。此外,稳定性参数略低于使用 Stable 分布重参数化模型找到的参数(较低的稳定性意味着更重的尾部)。

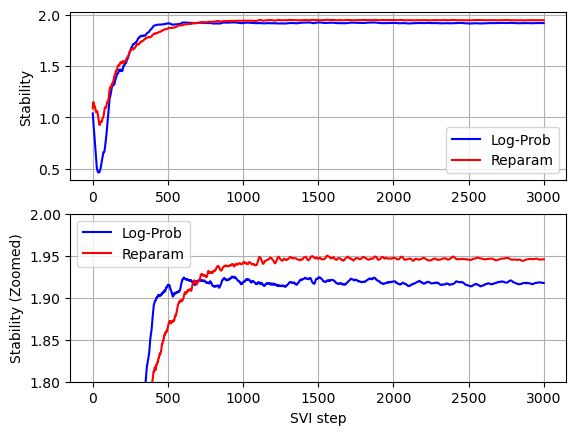

比较两个模型的收敛情况(参见下面的图),我们可以看到,在没有对 Stable 分布进行重参数化的情况下,稳定性参数收敛所需的迭代次数较少,但是由于没有对 Stable 分布进行重参数化时每次迭代的运行时间要高得多,因此总的运行时间显著更高。

[15]:

stability_with_log_prob = []

skew_with_log_prob = []

for stat in stats_with_log_prob:

stat = dict(stat)

stability_with_log_prob.append(stat['r_stability'].mean().item())

skew_with_log_prob.append(stat['r_skew'].mean().item())

stability = []

skew = []

for stat in stats:

stat = dict(stat)

stability.append(stat['r_stability'].mean().item())

skew.append(stat['r_skew'].mean().item())

[16]:

def plot_comparison(log_prob_values, reparam_values, xlabel, ylabel):

pyplot.plot(log_prob_values, color='b', label='Log-Prob')

pyplot.plot(reparam_values, color='r', label='Reparam')

pyplot.xlabel(xlabel)

pyplot.ylabel(ylabel)

pyplot.legend(loc='best')

pyplot.grid()

pyplot.subplot(2,1,1)

plot_comparison(stability_with_log_prob, stability, '', 'Stability')

pyplot.subplot(2,1,2)

plot_comparison(stability_with_log_prob, stability, 'SVI step', 'Stability (Zoomed)')

pyplot.ylim(1.8, 2)

[16]:

(1.8, 2.0)

[17]:

plot_comparison(skew_with_log_prob, skew, 'SVI step', 'Skew')