使用动态线性模型 (DLM) 进行预测¶

在状态空间模型中,动态线性模型 (DLM) 因其可解释性以及能够包含具有动态系数的回归变量而成为最受欢迎的模型之一。Harvey (1989) 和 Durbin and Koopman (2002) 等文献对这些模型进行了完整回顾。本笔记本介绍了通过 Pyro 和 Forecaster 模块构建原生 DLM 的方法。最后,它提供了一个扩展,用于包含灵活的系数先验。

另请参阅:- 预测 II:状态空间模型

工作流程¶

数据模拟

系数和响应的可视化

标准 DLM 训练和验证

后验比较

留出验证

在不同时间点使用系数先验的 DLM

后验比较

留出验证

[1]:

import matplotlib.pyplot as plt

import pandas as pd

import numpy as np

import torch

import pyro

import pyro.distributions as dist

import pyro.poutine as poutine

from pyro.contrib.forecast import ForecastingModel, Forecaster, eval_crps

from pyro.infer.reparam import LocScaleReparam

from pyro.ops.stats import quantile

%matplotlib inline

assert pyro.__version__.startswith('1.9.1')

pyro.set_rng_seed(20200928)

pd.set_option('display.max_rows', 500)

plt.style.use('fivethirtyeight')

数据模拟¶

假设我们在时间 \(t\) 有观测值 \(y_t\),满足

其中

\(x_t\) 是时间 \(t\) 的 P x 1 回归变量向量

\(\beta_t\) 是时间 \(t\) 的 P x 1 隐系数向量,服从随机游走分布

\(\epsilon\) 是时间 \(t\) 的噪声

然后我们在以下分布中模拟数据

[2]:

torch.manual_seed(20200101)

# number of predictors, total observations

p = 5

n = 365 * 3

# start, train end, test end

T0 = 0

T1 = n - 28

T2 = n

# initializing coefficients at zeros, simulate all coefficient values

beta0 = torch.empty(n, 1).normal_(0, 0.1).cumsum(0)

betas_p = torch.empty(n, p).normal_(0, 0.02).cumsum(0)

betas = torch.cat([beta0, betas_p], dim=-1)

# simulate regressors

covariates = torch.cat(

[torch.ones(n, 1), torch.randn(n, p) * 0.1],

dim=-1

)

# observation with noise

y = ((covariates * betas).sum(-1) + 0.1 * torch.randn(n)).unsqueeze(-1)

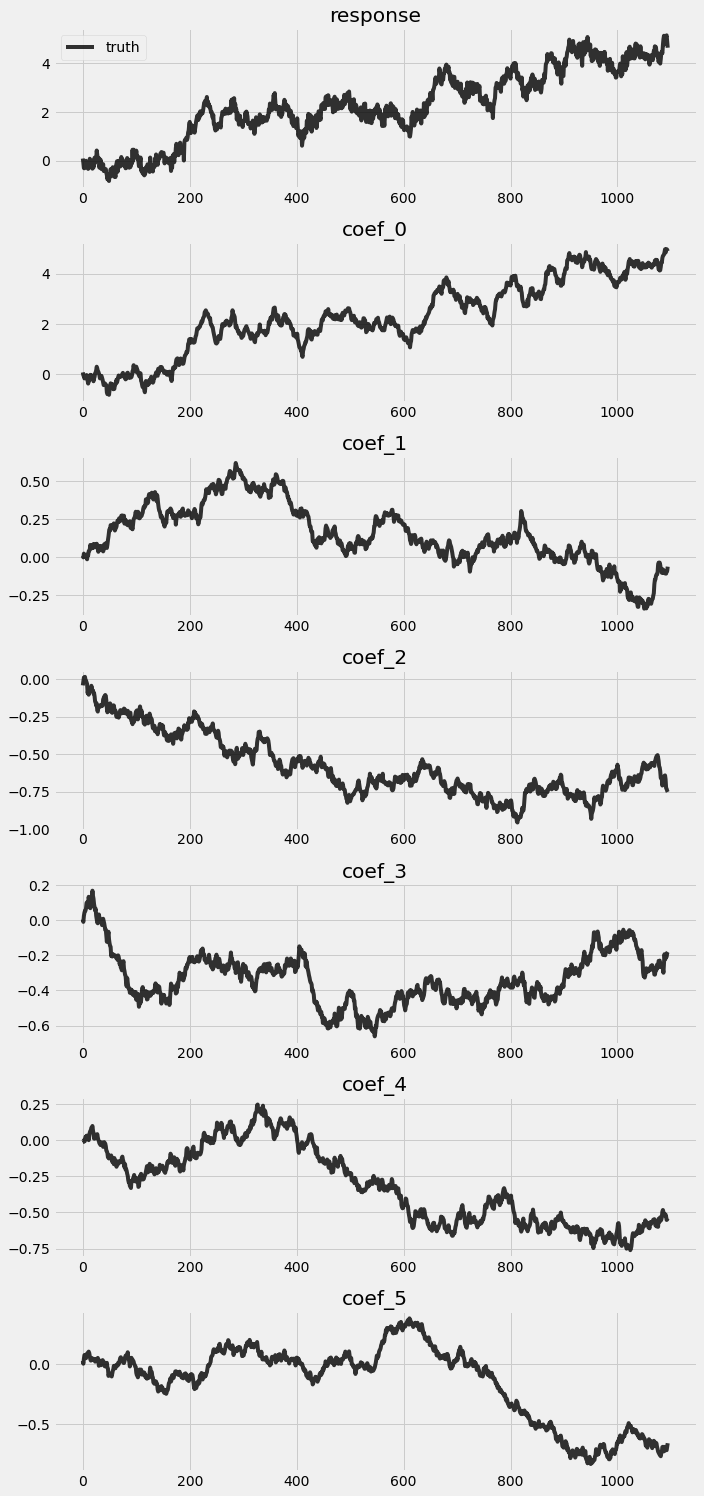

响应和系数的可视化¶

让我们看一下从前一个块模拟的真实值。

[3]:

fig, axes = plt.subplots(p + 2, 1, figsize=(10, 3 * (p + 2)))

for idx, ax in enumerate(axes):

if idx == 0:

axes[0].plot(y, 'k-', label='truth', alpha=.8)

axes[0].legend()

axes[0].set_title('response')

else:

axes[idx].plot(betas[:, idx - 1], 'k-', label='truth', alpha=.8)

axes[idx].set_title('coef_{}'.format(idx - 1))

plt.tight_layout()

训练和验证原生 DLM¶

让我们按照前面讨论的动态构建原生 DLM。

[4]:

class DLM(ForecastingModel):

def model(self, zero_data, covariates):

data_dim = zero_data.size(-1)

feature_dim = covariates.size(-1)

drift_scale = pyro.sample("drift_scale", dist.LogNormal(-10, 10).expand([feature_dim]).to_event(1))

with self.time_plate:

with poutine.reparam(config={"drift": LocScaleReparam()}):

drift = pyro.sample("drift", dist.Normal(torch.zeros(covariates.size()), drift_scale).to_event(1))

weight = drift.cumsum(-2) # A Brownian motion.

# record in model_trace

pyro.deterministic("weight", weight)

prediction = (weight * covariates).sum(-1, keepdim=True)

assert prediction.shape[-2:] == zero_data.shape

# record in model_trace

pyro.deterministic("prediction", prediction)

scale = pyro.sample("noise_scale", dist.LogNormal(-5, 10).expand([1]).to_event(1))

noise_dist = dist.Normal(0, scale)

self.predict(noise_dist, prediction)

[5]:

%%time

pyro.set_rng_seed(1)

pyro.clear_param_store()

model = DLM()

forecaster = Forecaster(

model,

y[:T1],

covariates[:T1],

learning_rate=0.1,

learning_rate_decay=0.05,

num_steps=1000,

)

INFO step 0 loss = 7.11372e+10

INFO step 100 loss = 174.352

INFO step 200 loss = 2.06682

INFO step 300 loss = 1.27919

INFO step 400 loss = 1.15015

INFO step 500 loss = 1.34206

INFO step 600 loss = 0.928436

INFO step 700 loss = 1.00953

INFO step 800 loss = 1.04599

INFO step 900 loss = 0.870245

CPU times: user 8.16 s, sys: 39.7 ms, total: 8.2 s

Wall time: 8.22 s

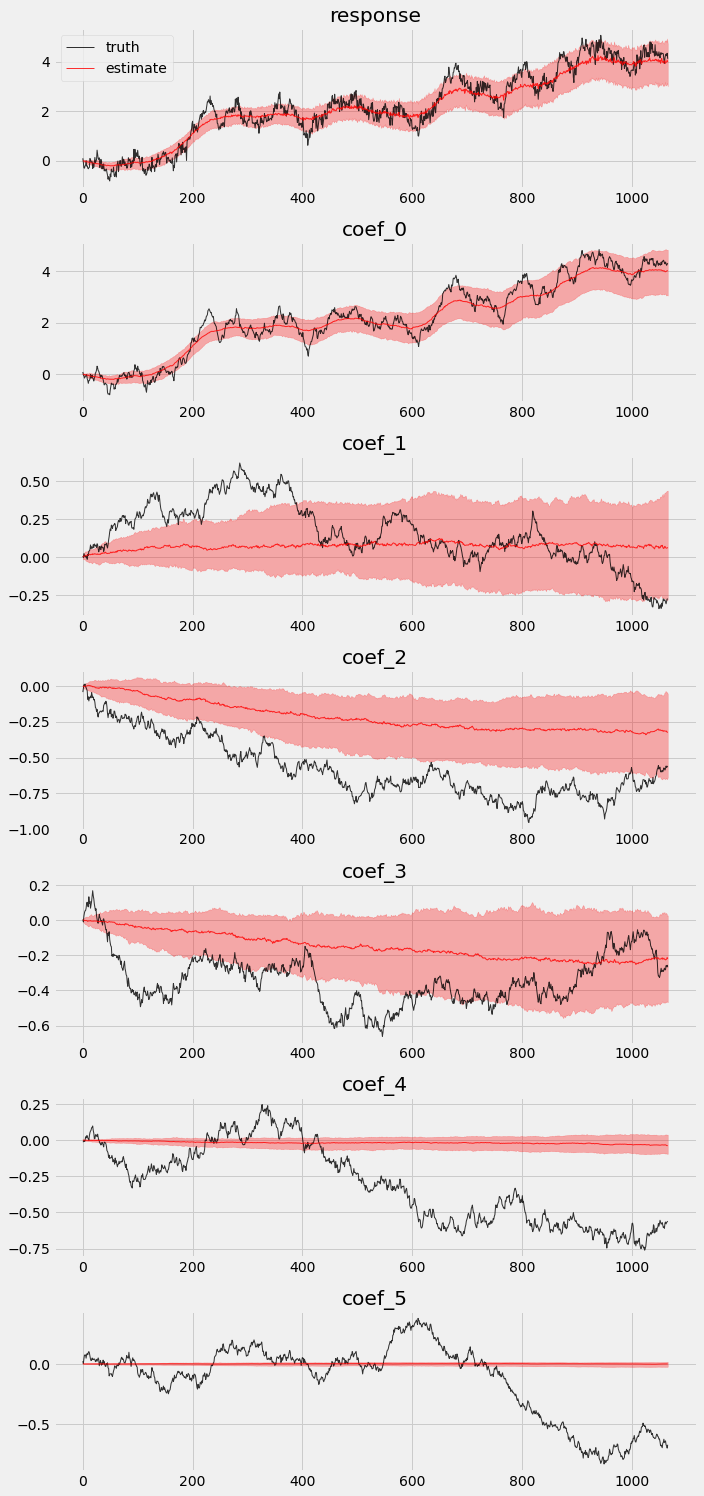

后验比较¶

我们提取样本内期间的后验,并将其与真实值进行比较。

[6]:

pyro.set_rng_seed(1)

# record all latent variables in a trace

with poutine.trace() as tr:

forecaster(y[:T1], covariates[:T1], num_samples=100)

# extract the values from the recorded trace

posterior_samples = {

name: site["value"]

for name, site in tr.trace.nodes.items()

if site["type"] == "sample"

}

我们也可以可视化样本内后验。

[7]:

# overlay estimations with truth

fig, axes = plt.subplots(p + 2, 1, figsize=(10, 3 * (p + 2)))

# posterior quantiles of latent variables

pred_p10, pred_p50, pred_p90 = quantile(posterior_samples['prediction'], (0.1, 0.5, 0.9)).squeeze(-1)

# posterior quantiles of latent variables

coef_p10, coef_p50, coef_p90 = quantile(posterior_samples['weight'], (0.1, 0.5, 0.9)).squeeze(-1)

for idx, ax in enumerate(axes):

if idx == 0:

axes[0].plot(y[:T1], 'k-', label='truth', alpha=.8, lw=1)

axes[0].plot(pred_p50, 'r-', label='estimate', alpha=.8, lw=1)

axes[0].fill_between(torch.arange(0, T1), pred_p10, pred_p90, color="red", alpha=.3)

axes[0].legend()

axes[0].set_title('response')

else:

axes[idx].plot(betas[:T1, idx - 1], 'k-', label='truth', alpha=.8, lw=1)

axes[idx].plot(coef_p50[:, idx - 1], 'r-', label='estimate', alpha=.8, lw=1)

axes[idx].fill_between(torch.arange(0, T1), coef_p10[:, idx-1], coef_p90[:, idx-1], color="red", alpha=.3)

axes[idx].set_title('coef_{}'.format(idx - 1))

plt.tight_layout()

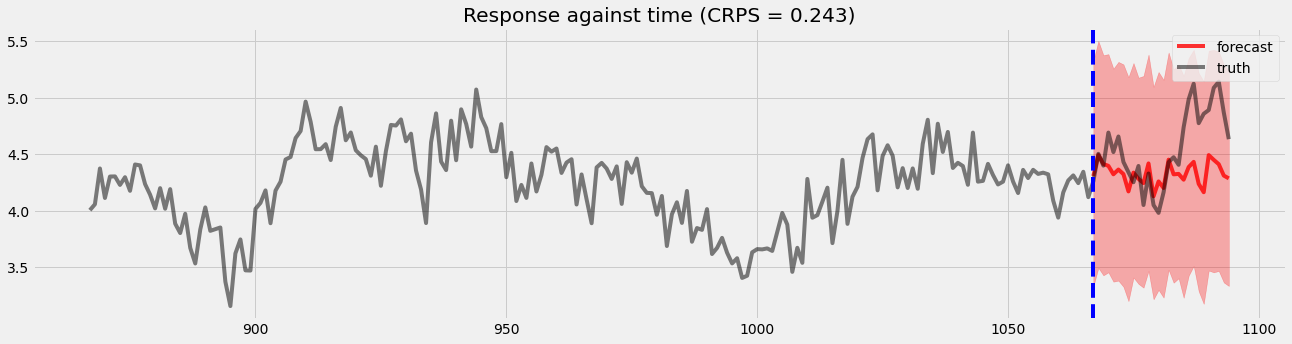

我们可以看到,在原生模型中并非所有系数都能被恢复。

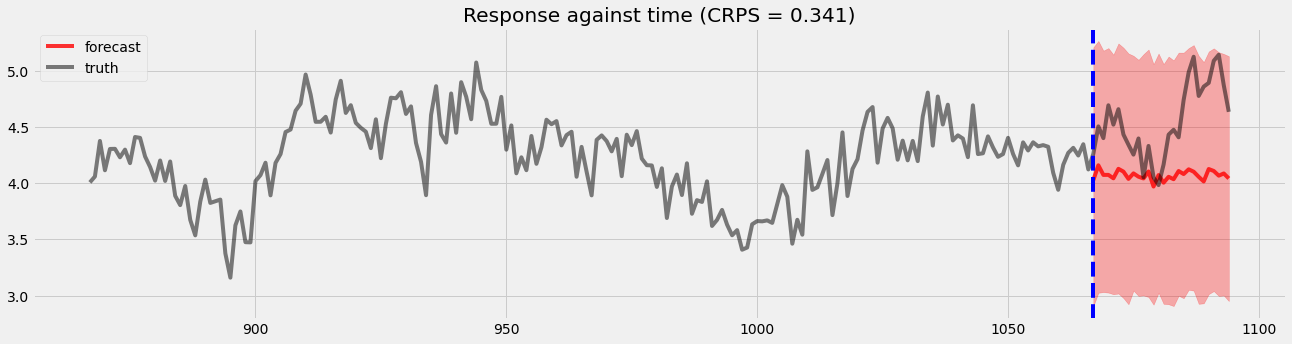

留出验证¶

在这里,我们将可视化留出验证结果以便后续比较。

[8]:

pyro.set_rng_seed(1)

samples = forecaster(y[:T1], covariates, num_samples=1000)

p10, p50, p90 = quantile(samples, (0.1, 0.5, 0.9)).squeeze(-1)

crps = eval_crps(samples, y[T1:])

plt.figure(figsize=(20, 5))

plt.fill_between(torch.arange(T1, T2), p10, p90, color="red", alpha=.3)

plt.plot(torch.arange(T1, T2), p50, 'r-', label='forecast', alpha=.8)

plt.plot(np.arange(T1 - 200, T2), y[T1 - 200:T2], 'k-', label='truth', alpha=.5)

plt.title("Response against time (CRPS = {:0.3g})".format(crps))

plt.axvline(T1, color='b', linestyle='--')

plt.legend(loc="best");

在不同时间点使用系数先验训练 DLM¶

有时用户可能对某个时间点的某些系数有先验信念。这在建模者可以为这些系数设置信息性先验的情况下很有用。为了说明,我们创建一些简单的均匀分布的时间点,并使用已知值 \(B_t\) 在这些点上设置先验,如下所示

其中 \(t \in [t_1, t_2, ... t_n]\) 且 \([t_1, t_2, ... t_n]\) 是我们具有经验结果的时间点。

[9]:

# let's provide some priors

time_points = np.concatenate((

np.arange(300, 320),

np.arange(600, 620),

np.arange(900, 920),

))

# broadcast on time-points

priors = betas[time_points, 1:]

[10]:

print(time_points.shape, priors.shape)

(60,) torch.Size([60, 5])

模型训练¶

现在,让我们构建新的 DLM,它允许用户在某些时间点导入系数先验。

[11]:

class DLM2(ForecastingModel):

def model(self, zero_data, covariates):

data_dim = zero_data.size(-1)

feature_dim = covariates.size(-1)

drift_scale = pyro.sample("drift_scale", dist.LogNormal(-10, 10).expand([feature_dim]).to_event(1))

with self.time_plate:

with poutine.reparam(config={"drift": LocScaleReparam()}):

drift = pyro.sample("drift", dist.Normal(torch.zeros(covariates.size()), drift_scale).to_event(1))

weight = drift.cumsum(-2) # A Brownian motion.

# record in model_trace

pyro.deterministic("weight", weight)

# This is the only change from the simpler DLM model.

# We inject prior terms as if they were likelihoods using pyro observe statements.

for tp, prior in zip(time_points, priors):

pyro.sample("weight_prior_{}".format(tp), dist.Normal(prior, 0.5).to_event(1), obs=weight[..., tp:tp+1, 1:])

prediction = (weight * covariates).sum(-1, keepdim=True)

assert prediction.shape[-2:] == zero_data.shape

# record in model_trace

pyro.deterministic("prediction", prediction)

scale = pyro.sample("noise_scale", dist.LogNormal(-5, 10).expand([1]).to_event(1))

noise_dist = dist.Normal(0, scale)

self.predict(noise_dist, prediction)

[12]:

%%time

pyro.set_rng_seed(1)

pyro.clear_param_store()

model = DLM2()

forecaster2 = Forecaster(

model,

y[:T1],

covariates[:T1],

learning_rate=0.1,

learning_rate_decay=0.05,

num_steps=1000,

)

INFO step 0 loss = 7.11372e+10

INFO step 100 loss = 105.237

INFO step 200 loss = 2.21884

INFO step 300 loss = 1.70493

INFO step 400 loss = 1.64291

INFO step 500 loss = 1.80583

INFO step 600 loss = 0.903905

INFO step 700 loss = 1.25712

INFO step 800 loss = 1.10254

INFO step 900 loss = 0.926691

CPU times: user 36.6 s, sys: 316 ms, total: 36.9 s

Wall time: 37.2 s

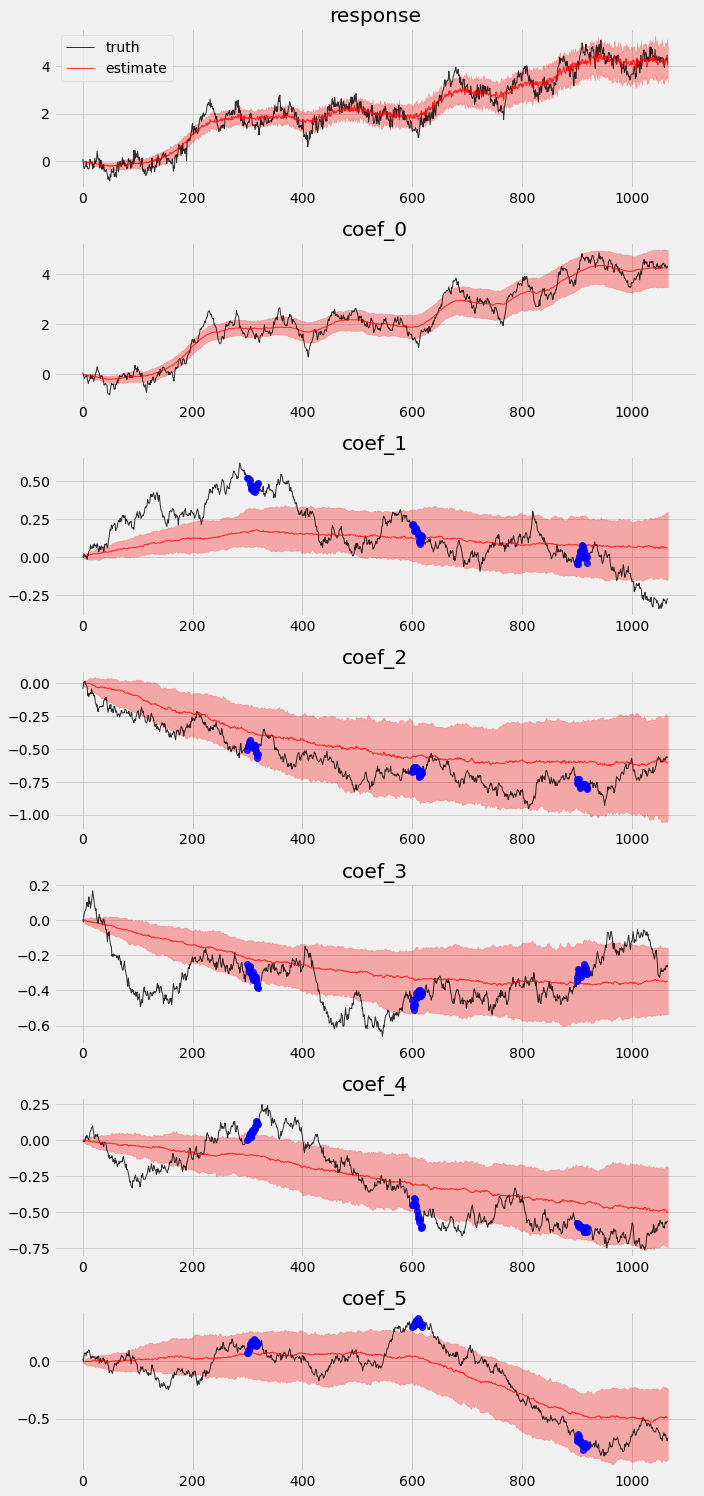

后验比较¶

最后,让我们重复前一节中的练习,检查样本内后验和留出验证。

[13]:

pyro.set_rng_seed(1)

with poutine.trace() as tr:

forecaster2(y[:T1], covariates[:T1], num_samples=100)

posterior_samples2 = {

name: site["value"]

for name, site in tr.trace.nodes.items()

if site["type"] == "sample"

}

[14]:

# overlay estimations with truth

fig, axes = plt.subplots(p + 2, 1, figsize=(10, 3 * (p + 2)))

# posterior quantiles of latent variables

pred_p10, pred_p50, pred_p90 = quantile(posterior_samples2['prediction'], (0.1, 0.5, 0.9)).squeeze(-1)

# posterior quantiles of latent variables

coef_p10, coef_p50, coef_p90 = quantile(posterior_samples2['weight'], (0.1, 0.5, 0.9)).squeeze(-1)

for idx, ax in enumerate(axes):

if idx == 0:

axes[0].plot(y[:T1], 'k-', label='truth', alpha=.8, lw=1)

axes[0].plot(pred_p50, 'r-', label='estimate', alpha=.8, lw=1)

axes[0].fill_between(torch.arange(0, T1), pred_p10, pred_p90, color="red", alpha=.3)

axes[0].legend()

axes[0].set_title('response')

else:

axes[idx].plot(betas[:T1, idx - 1], 'k-', label='truth', alpha=.8, lw=1)

axes[idx].plot(coef_p50[:, idx - 1], 'r-', label='estimate', alpha=.8, lw=1)

if idx >= 2:

axes[idx].plot(time_points, priors[:, idx-2], 'o', color='blue', alpha=.8, lw=1)

axes[idx].fill_between(torch.arange(0, T1), coef_p10[:, idx-1], coef_p90[:, idx-1], color="red", alpha=.3)

axes[idx].set_title('coef_{}'.format(idx - 1))

plt.tight_layout()

留出验证¶

[15]:

pyro.set_rng_seed(1)

samples2 = forecaster2(y[:T1], covariates, num_samples=1000)

p10, p50, p90 = quantile(samples2, (0.1, 0.5, 0.9)).squeeze(-1)

crps = eval_crps(samples2, y[T1:])

print(samples2.shape, p10.shape)

plt.figure(figsize=(20, 5))

plt.fill_between(torch.arange(T1, T2), p10, p90, color="red", alpha=.3)

plt.plot(torch.arange(T1, T2), p50, 'r-', label='forecast', alpha=.8)

plt.plot(np.arange(T1 - 200, T2), y[T1 - 200:T2], 'k-', label='truth', alpha=.5)

plt.title("Response against time (CRPS = {:0.3g})".format(crps))

plt.axvline(T1, color='b', linestyle='--')

plt.legend(loc="best");

torch.Size([1000, 28, 1]) torch.Size([28])

我们可以看到,在系数运动检测和留出验证方面都有明显的改进。

结论¶

我们展示了如何使用 Pyro 创建一个经典的 DLM,它提供了不错的预测结果。

通过注入先验,我们在获得更准确的系数和预测方面改进了模型。

参考文献¶

Harvey, C. A. (1989). Forecasting, Structural Time Series and the Kalman Filter, Cambridge University Press.

Durbin, J., Koopman, S. J.. (2001). Time Series Analysis by State Space Methods, Oxford Statistical Science Series

Scott, S. L., and Varian, H. (2015). “Inferring Causal Impact using Bayesian Structural Time-Series Models” The Annals of Applied Statistics, 9(1), 247–274.

Moore, D., Burnim, J, and the TFP Team (2019). “Structural Time Series modeling in TensorFlow Probability” Available at https://blog.tensorflowcn.cn/2019/03/structural-time-series-modeling-in.html